Have any questions? Contact us!

Join our team!

Request a free quote or consultation

A performance bond in construction is a surety bond that guarantees a contractor will complete a project according to contract terms. It protects project owners by providing financial compensation if the contractor fails to fulfill obligations, with the surety company assuming responsibility for completion or costs.

Construction projects involve significant financial risk. Project owners invest millions into buildings, infrastructure, and facilities—and they need assurance their contractor will actually finish the job.

That’s where performance bonds come in.

These financial guarantees protect project owners from contractor default, ensuring projects reach completion even when things go wrong. But how exactly do they work? What do they cost? And when are they required?

Understanding Performance Bonds: The Basics

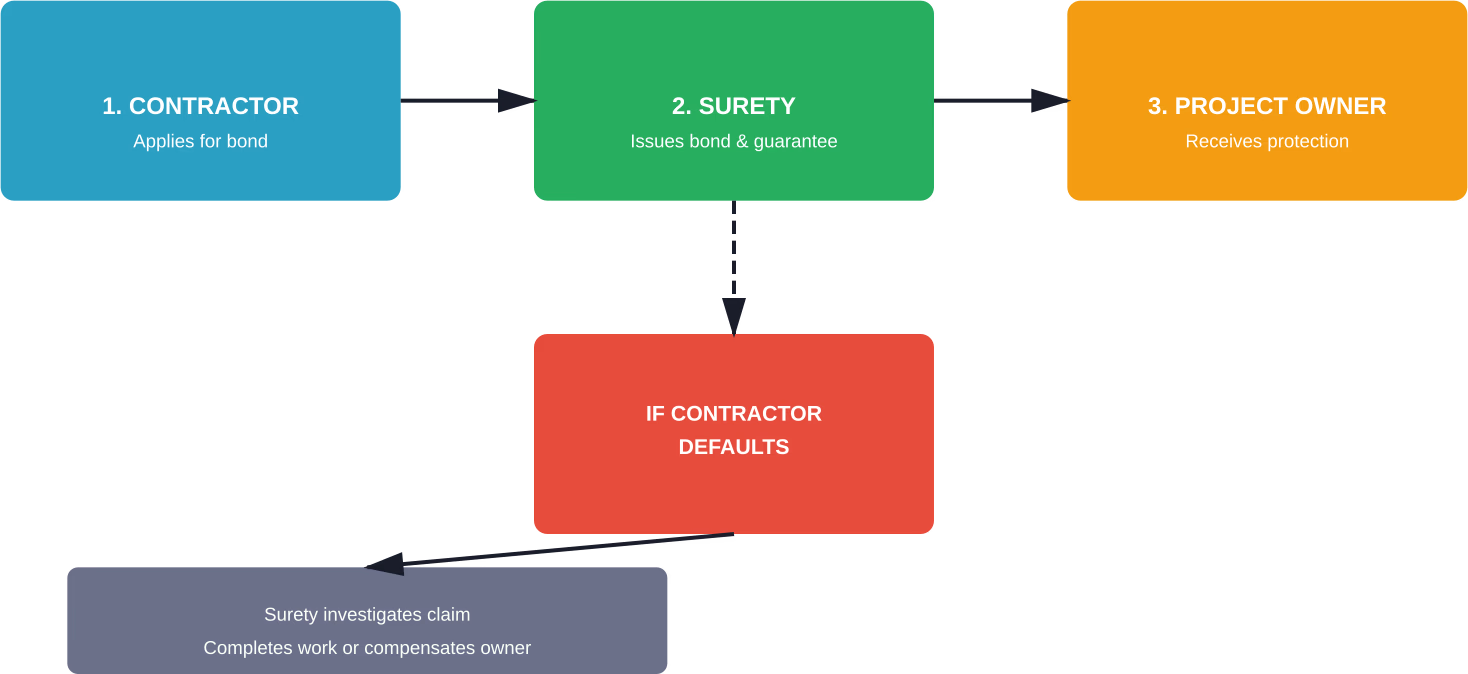

A performance bond is a three-party agreement between the principal (contractor), the surety company, and the obligee (project owner). According to the Surety & Fidelity Association of America, surety bonds are written agreements, often required by law, to guarantee performance or payment of another company’s obligation under a separate contract.

Here’s the thing though—performance bonds aren’t insurance policies. Insurance protects the policyholder from unexpected losses. Performance bonds protect the project owner from the contractor’s failure to perform.

The surety company essentially vets the contractor’s capability to complete the specified project on behalf of the project owner. When a surety agrees to bond a contractor, they’re vouching for that contractor’s financial stability, technical competence, and track record.

The Three Parties Involved

Every performance bond involves these three entities:

- Principal: The contractor or company performing the work

- Surety: The insurance or bonding company guaranteeing the work

- Obligee: The project owner or entity requiring the bond

If the principal fails to complete the project according to contract terms, the obligee can make a claim against the bond. The surety then investigates and, if the claim is valid, takes action to remedy the situation.

How Performance Bonds Work in Construction

When a contractor bids on a bonded project, they must secure a performance bond before work begins. The process typically follows this sequence:

First, the contractor applies to a surety company. The surety evaluates the contractor’s financial health, experience, and capacity to complete the project. This underwriting process examines balance sheets, past project performance, and available resources.

Once approved, the surety issues the bond for a premium—typically 1-3% of the total contract amount, according to industry data. The bond guarantees the full contract value, providing the project owner with financial protection equal to the entire project cost.

Now, if the contractor fails to meet contractual obligations—whether through abandonment, bankruptcy, or inability to complete the work—the project owner files a claim with the surety company.

What Happens After a Claim

The surety has several options when faced with a valid claim:

- Complete the work: Hire another contractor to finish the project

- Pay the bond amount: Compensate the owner up to the bond’s penal sum

- Assist the original contractor: Provide resources to help them complete the work

Research from academic sources notes that the nature of performance bonds can be perplexed and occasionally subject to abuse. Issues arise from archaic language, dated contract wordings, and loopholes that enable fraudulent claims.

Performance Bond vs Payment Bond: Key Differences

Performance bonds often get confused with payment bonds, but they serve distinct purposes. Many construction projects require both.

| Aspect | Performance Bond | Payment Bond |

|---|---|---|

| Protects | Project owner | Subcontractors and suppliers |

| Guarantees | Project completion per contract terms | Payment for labor and materials |

| Claimants | Project owner | Subcontractors, suppliers, laborers |

| Purpose | Ensure work gets finished | Ensure workers get paid |

| Typical Amount | 100% of contract value | 100% of contract value |

Payment bonds protect the supply chain. If a general contractor fails to pay subcontractors or material suppliers, those parties can file claims against the payment bond. This prevents mechanic’s liens from being filed against the property.

Performance bonds protect project completion. They ensure the facility actually gets built.

Federal Requirements: The Miller Act

According to the Associated General Contractors of America, the Miller Act—enacted in 1935—requires performance and payment bonds on federal construction projects exceeding $100,000. This legislation has successfully protected the interests of the federal government, taxpayers, and subcontractors for over 90 years.

The Federal Acquisition Regulation specifies that contractors must furnish both bonds before contract award. The penal sum typically equals 100% of the contract price, providing full protection for the project value.

Real talk: the Miller Act set the standard that many state and local governments have since adopted. Most states have “Little Miller Acts” requiring bonds on public projects above certain thresholds.

Bond Amounts and Thresholds

Federal regulations establish specific requirements:

- Contracts over $100,000 require performance and payment bonds

- Bid bonds typically equal 20% of the bid price (capped at $3 million)

- Performance bonds usually equal 100% of the contract amount

- Payment bonds also typically equal 100% of contract value

For cost-reimbursement contracts, bond requirements are typically waived. However, fixed-price construction subcontracts over $40,000 under cost-type prime contracts require the prime contractor to obtain bonds from subcontractors.

What Performance Bonds Cost

Performance bond premiums generally range from 1-3% of the total contract amount, based on data from construction surety providers. But that’s just the baseline.

Several factors affect the actual cost:

- Contractor’s financial strength: Strong balance sheets and healthy cash flow reduce premiums. Surety companies examine working capital, assets, liabilities, and financial ratios during underwriting.

- Project size and complexity: Larger projects or technically challenging work increase risk, raising premiums. A $10 million hospital renovation will cost more to bond than a $500,000 warehouse.

- Contractor’s experience: Track record matters. Contractors with successful project histories and relevant experience pay lower premiums than those entering new territory.

- Project location: Geographic factors influence risk assessment. Remote locations or regions with labor shortages may increase costs.

Calculating Premium on Real Projects

For a $2 million commercial building project with a 2% premium rate, the performance bond costs $40,000. That’s a one-time fee paid at bond issuance, not an annual premium like traditional insurance.

For a $500,000 renovation with a contractor who has strong financials and relevant experience, a 1.5% rate means $7,500 for the bond.

These costs get factored into the contractor’s bid. They’re legitimate project expenses that ultimately flow through to the project owner.

How Contractors Obtain Performance Bonds

Securing a performance bond requires preparation. Contractors can’t walk in the day before a project starts and expect immediate approval.

The process begins with establishing a relationship with a surety company or surety bond agent. Many contractors work with specialized bond producers who represent multiple surety companies and can find the best fit.

The Underwriting Process

Surety underwriters evaluate three key areas—often called the “Three C’s”:

- Character: The contractor’s integrity, reputation, and track record. Sureties want to see completed projects, satisfied clients, and ethical business practices.

- Capacity: Technical ability and resources to complete the specific project. Can this contractor actually build what they’re bidding? Do they have the equipment, workforce, and expertise?

- Capital: Financial strength to support the work. Strong working capital, manageable debt, and healthy cash flow demonstrate capacity to handle project demands and potential setbacks.

Contractors typically need to provide:

- Audited financial statements (often the past three years)

- Work-in-progress schedules

- Bank references

- Project resumes and references

- Business and personal tax returns

- Details about the specific project requiring the bond

Underwriting can take anywhere from a few days to several weeks, depending on the contractor’s preparedness and the project’s complexity.

Bonding Capacity Limitations

Surety companies establish bonding capacity limits for each contractor—essentially a credit line for bonds. This capacity depends on the contractor’s financial strength and typically ranges from 5-15 times working capital.

A contractor with $2 million in working capital might have bonding capacity of $10-20 million for aggregate work under bond. This limits how many bonded projects they can carry simultaneously.

That said, contractors can increase bonding capacity by strengthening their balance sheets, completing projects successfully, and building relationships with sureties over time.

When Performance Bonds Are Required

Beyond federal projects under the Miller Act, performance bonds are commonly required on:

- State and local government projects: Most states mandate bonds on public construction above certain dollar thresholds—often $50,000 to $100,000.

- Large private projects: Developers, corporations, and institutions frequently require bonds on major construction to protect their investments.

- Projects with public funds: Any construction involving taxpayer money typically requires bonding to ensure accountability.

- Projects with complex financing: Lenders often require performance bonds to protect their financial interests in construction loans.

| Project Type | Bond Requirement | Typical Threshold |

|---|---|---|

| Federal Construction | Mandatory (Miller Act) | Over $100,000 |

| State/Local Public Works | Usually mandatory | $50,000-$100,000+ |

| Private Commercial | Project owner’s discretion | Varies widely |

| Residential Construction | Rarely required | N/A |

| Design-Build Projects | Often required | Varies by owner |

Residential construction rarely requires performance bonds except on large multifamily developments or projects involving public housing funds.

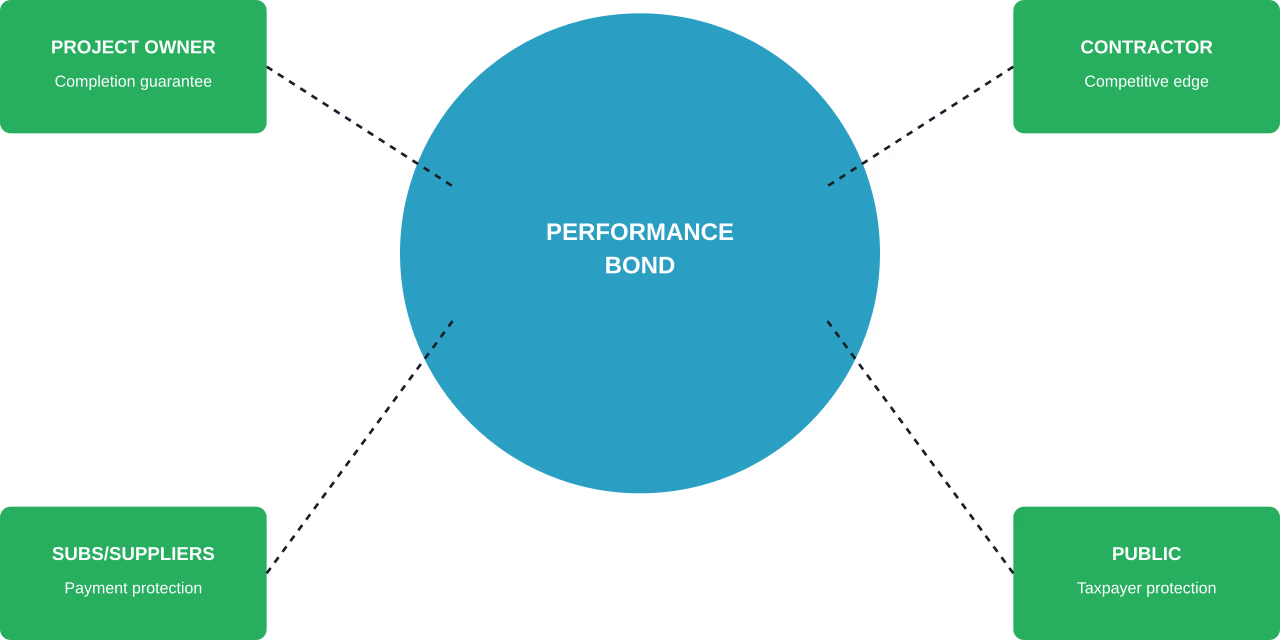

Benefits of Performance Bonds

Performance bonds create value for all parties involved in construction projects—not just project owners.

For Project Owners

The protection is straightforward. If the contractor fails, the surety ensures project completion or provides financial compensation up to the bond amount. This prevents abandoned projects, protects investments, and maintains project schedules.

But there’s another benefit: pre-qualification. When a surety agrees to bond a contractor, they’ve verified that contractor’s capability. Project owners gain confidence they’re working with financially stable, technically competent contractors.

For Contractors

Bonds open doors. Many lucrative projects require them, so bonding capacity directly expands business opportunities.

Bonds also demonstrate credibility. Being bondable signals financial strength and reliability—powerful differentiators in competitive bidding.

Additionally, performance bonds can actually reduce project disputes. The surety’s oversight and involvement provide a neutral third party that can help resolve issues before they escalate.

For Subcontractors and Suppliers

When paired with payment bonds, performance bonds create a safer business environment. Subcontractors and suppliers gain protection against non-payment, reducing their risk when working with general contractors they don’t know well.

Reduce Performance Bond Risk Now

A bond only pays when something goes wrong. The better move is to cut the chances of default in the first place. Powerkh pressure-tests the parts of the job that typically fail – incomplete design, weak interfaces, and details that don’t survive installation – so you don’t carry that risk into delivery. They look at how the design will behave under real site conditions, not just how it reads on paper. That gives you a clear view of what could trigger delay, rework, or non-performance before it becomes a claim.

Remove Failure Points Before Construction

What you get with Powerkh:

- Pinpointed areas where the job is likely to break during execution

- Clear view of unresolved interfaces that can stop progress

- Early fixes to details that won’t install as planned

- Better alignment between issued design and on-site work

- Fewer triggers for claims, delays, and bond exposure

If you’re carrying bond risk, reach out to Powerkh and deal with it before it turns into a claim.

Common Misconceptions About Performance Bonds

Several myths persist about how performance bonds work:

- Misconception #1: Performance bonds are insurance. They’re not. Insurance protects the policyholder from unexpected losses. Performance bonds guarantee the contractor’s obligations to the project owner. If the surety pays out, they pursue reimbursement from the contractor through the indemnity agreement.

- Misconception #2: The surety always finishes the work. Not necessarily. The surety has multiple remediation options, including helping the original contractor complete the work, hiring a new contractor, or paying the bond amount. Their choice depends on what’s most cost-effective.

- Misconception #3: Once bonded, always bonded. Bonding capacity isn’t permanent. Sureties continuously monitor bonded contractors’ financial health and project performance. Financial deterioration or project problems can reduce or eliminate bonding capacity.

- Misconception #4: All contractors can get bonded. Many contractors can’t obtain bonds due to weak financials, poor credit, inadequate experience, or troubled project histories. Bonding serves as a qualification filter.

Challenges and Criticisms

Academic research points out legitimate concerns with performance bond systems. Studies note that interpretation issues, drafting problems, and archaic language in bond contracts create disputes and enable abuse.

The instrument’s complexity—whether it’s technically a “bond” or a “guarantee” in legal terms—creates confusion that sometimes triggers major disputes. These terms get used intermittently but carry different obligation values under law.

Another concern: suspected fraudulent calls by beneficiaries. Loopholes in bond contracts sometimes make it easy for project owners to make questionable claims. Several professional bodies have expressed concerns about potential abuse.

Standardized systems and structures would help create uniformity in application and reduce these problems. The industry continues working toward clearer, more consistent bonding practices.

Conclusion

Performance bonds serve as essential risk management tools in construction. They protect project owners from contractor default, give contractors access to larger opportunities, and create accountability that benefits the entire industry.

Understanding how these bonds work—their costs, requirements, and limitations—helps both contractors and project owners navigate construction projects more effectively. The surety bond system has protected construction interests for over 90 years, evolving to meet the demands of increasingly complex projects.

For contractors, maintaining strong financials and building relationships with surety companies expands business opportunities. For project owners, requiring performance bonds provides peace of mind that projects will reach completion regardless of contractor circumstances.

If you’re preparing to bid on a bonded project or considering whether to require bonds on your construction work, consult with a qualified surety bond professional who can assess your specific situation and provide tailored guidance.

Frequently Asked Questions

What’s the difference between a bid bond and a performance bond?

A bid bond guarantees that if a contractor wins a bid, they’ll sign the contract and provide the required performance and payment bonds. Bid bonds typically equal 10-20% of the bid amount. Performance bonds guarantee the contractor will complete the actual work and typically equal 100% of the contract value. Bid bonds protect the procurement process; performance bonds protect project execution.

Can a contractor get a performance bond with bad credit?

It’s difficult but not impossible. Sureties primarily evaluate financial strength, not personal credit scores. However, poor credit often reflects financial problems that affect bonding eligibility. Contractors with credit challenges might access bonds through specialized programs, by providing additional collateral, or by partnering with financially stronger entities. Building financial strength and demonstrating successful project completion are the best paths forward.

Who pays for the performance bond?

The contractor pays the bond premium, but that cost gets incorporated into their project bid. Ultimately, the project owner pays for the bond as part of the total project cost. The premium is a legitimate, necessary business expense for bonded work.

How long does a performance bond last?

Performance bonds remain in effect until the contract is fulfilled and accepted by the project owner. This includes the construction period plus any warranty period specified in the contract. The bond doesn’t expire on a specific date – it terminates when contractual obligations are satisfied and the surety receives written confirmation of project completion and acceptance.

What happens if a bonded contractor goes bankrupt?

The surety company steps in to ensure project completion. They might provide financing for the contractor to continue, hire a new contractor to complete the work, or pay out the bond amount to the project owner. The surety has legal obligation under the bond to remedy the situation. The contractor (and any indemnitors who signed the indemnity agreement) remain liable to reimburse the surety for any costs incurred.

Are performance bonds required on all construction projects?

No. Federal projects over $100,000 require them under the Miller Act. Most states require bonds on public projects above certain thresholds. Private projects don’t legally require bonds, though project owners often demand them as a condition of contract award. Residential construction rarely involves performance bonds except on large developments.

Can a contractor be bonded for multiple projects simultaneously?

Yes, but their aggregate bonded work cannot exceed their bonding capacity. Sureties establish limits based on the contractor’s financial strength – typically 5-15 times working capital. A contractor with $1 million in working capital might handle $5-10 million in simultaneous bonded work. As projects complete, capacity becomes available for new bonds.

Our Case Studies

We have handled 200+ BIM & VDC projects for commercial, industrial, and residential sectors.

Our work includes:

Formwork design automation

Our client from

California, USA

Suspended ceiling design automation

Our client from

New York, USA

Wall framing design automation

Our client from

California, USA