¿Tiene alguna pregunta? Póngase en contacto con nosotros

¡Únete a nuestro equipo!

Solicitar presupuesto o consulta gratuita

Job costing in construction is a method of tracking and allocating all costs—labor, materials, equipment, and overhead—to individual projects, enabling contractors to monitor profitability, compare actual expenses against estimates, and make data-driven decisions that protect margins and improve future bidding accuracy.

Margins in construction are razor-thin. A single project can show impressive revenue numbers while quietly bleeding cash through untracked expenses, scope creep, and underestimated labor burden.

Here’s the thing though—a contractor can show $200K in annual profit while losing money on 40 percent of their jobs. The profitable projects mask the losers.

Job costing fixes this visibility problem by breaking down every expense tied to a specific project. It tells contractors which jobs make money and which ones don’t, before it’s too late to correct the course.

What Is a Job Costing in Construction?

Job costing is an accounting method that tracks actual costs for individual construction projects with unique scopes. Instead of lumping all company expenses into one bucket, job costing assigns labor hours, material purchases, equipment usage, and overhead to specific jobs.

This creates a clear financial picture for each project. Contractors can compare actual costs against their original estimates, identify where money is being spent, and determine whether a job will hit its target profit margin.

The process works because construction projects are inherently unique. A commercial hotel build requires different materials, labor skills, and timelines than a residential kitchen remodel. Standard costing—which uses predetermined benchmarks—doesn’t capture this variability.

Job costing, by contrast, adapts to each project’s reality. If drywall was estimated at $2 per square foot but actually cost $2.25, that variance gets flagged immediately. Contractors can then investigate whether the issue was supplier pricing, installation inefficiency, or estimation error.

Key Characteristics of Construction Job Costing

Several features distinguish job costing from other accounting methods:

- Project-specific tracking: Every cost gets assigned to a particular job number or code

- Real-time visibility: Costs are recorded as they occur, not retroactively

- Variance analysis: Actual expenses are continuously compared against estimates

- Multi-dimensional categorization: Costs are broken down by type (labor, materials, equipment) and phase (site prep, framing, finishing)

The math is simple. If a $500,000 project has a 15 percent profit margin, the target profit is $75,000. A 5 percent cost overrun drops that profit to $50,000—a third of the expected return vanishes.

Core Components of Job Costing

Construction job costing breaks expenses into four primary categories. Understanding each component—and how it behaves—is essential for accurate tracking.

Direct Labor Costs

Direct labor includes wages paid to workers who physically build the project: framers, electricians, plumbers, and finishers. But the actual cost extends far beyond base hourly rates.

Labor burden adds 24-70% to base wages. Beyond direct wages, payroll taxes, benefits, workers’ compensation insurance, and paid time off create fully-burdened labor costs that many contractors underestimate when bidding projects.

A worker earning $25 per hour might actually cost the company $35-40 per hour after burden. That $10-15 difference compounds across thousands of labor hours on a large project.

Tracking labor accurately requires:

- Time cards or digital tracking systems that capture hours by project and task

- Regular updates to burden rates as insurance costs and benefit expenses change

- Allocation of travel time, setup time, and cleanup time to the correct jobs

Materials and Supplies

Materials represent the physical components that become part of the finished structure. This category includes lumber, concrete, drywall, fixtures, finishes, and consumables like fasteners and adhesives.

Material costs fluctuate based on market conditions, supplier relationships, and order timing. A quote received during estimation might not match the actual purchase price months later when construction begins.

Effective material tracking requires:

- Purchase orders tied to specific job codes

- Delivery tickets that confirm quantities received

- Waste tracking to identify losses from damage, theft, or over-ordering

- Reconciliation between estimated quantities and actual usage

Equipment and Tool Costs

Equipment costs include both owned machinery and rented tools. For owned equipment, contractors must allocate depreciation, maintenance, fuel, and operator wages. For rentals, the daily or weekly rate gets charged directly to the project.

Without proper tracking, it’s difficult to determine if equipment investments are being maximized or if rental costs could be reduced through better scheduling and utilization.

A $50,000 excavator might serve multiple projects. Job costing allocates equipment hours to each job based on actual usage, ensuring that projects bear their fair share of equipment expense.

Indirect Costs and Overhead

Indirect costs typically account for 15-30% of total project costs (though they can range from 10% to 40% depending on project complexity and sector). These expenses support project delivery but can’t be directly attributed to a single task or material.

Overhead falls into two categories:

- Project-level overhead: Permits, site utilities, temporary fencing, dumpsters, project management salaries, and insurance specific to the job.

- Company-level overhead: Office rent, administrative salaries, accounting fees, marketing, and general liability insurance.

Contractors typically allocate company overhead to jobs using a percentage of direct costs or as a fixed markup. The allocation method matters less than consistency—using the same approach across all projects enables meaningful comparisons.

Job Costing vs Other Accounting Methods

Construction companies have several accounting approaches available. Understanding the differences helps clarify why job costing works best for most contractors.

| Method | Definition | Lo mejor para | Ejemplo

|

|---|---|---|---|

| Job Costing | Tracks actual costs for projects with unique scopes | Custom construction projects | Commercial hotel build |

| Standard Costing | Compares actual costs to predetermined benchmarks | Manufacturing with predictable inputs | Production line assembly |

| Process Costing | Averages costs across identical units | High-volume identical products | Prefab panel manufacturing |

| Project Costing | Broad approach to tracking larger initiatives | Multi-phase developments | Mixed-use property complex |

Standard costing works for businesses with predictable, repeatable processes. A factory making identical widgets can establish precise cost benchmarks because materials, labor, and overhead remain constant.

Construction doesn’t work that way. Site conditions vary. Material prices fluctuate. Labor productivity changes based on weather, crew experience, and project complexity.

Job costing accommodates this variability by tracking what actually happens rather than what should theoretically happen.

How to Implement Job Costing

Setting up an effective job costing system requires both process design and technology infrastructure. The following steps provide a framework for implementation.

Step 1: Establish Job Cost Codes

Cost codes create the organizational structure for tracking expenses. Most contractors use a hierarchical system that breaks down projects by division, category, and task.

A common structure follows the Construction Specifications Institute (CSI) MasterFormat:

- 01: General Conditions (permits, insurance, temporary facilities)

- 03: Concrete (formwork, reinforcement, placement)

- 06: Wood, Plastics, and Composites (rough carpentry, finish carpentry)

- 09: Finishes (drywall, painting, flooring)

Within each division, subcodes identify specific tasks. Code 06-1000 might represent rough carpentry labor, while 06-1001 captures rough carpentry materials.

The challenge intensifies as businesses scale. A $10 million contractor managing five simultaneous projects faces different complexity than a $50 million firm running 30 jobs across multiple states with varying union requirements and prevailing wage obligations.

Step 2: Create Detailed Estimates

Job costing only works when actual costs can be compared against accurate estimates. The estimation process establishes baseline expectations for labor hours, material quantities, equipment needs, and overhead allocation.

Detailed estimates break down every aspect of the work:

- Quantity takeoffs from plans and specifications

- Labor productivity rates based on historical data

- Material pricing from current supplier quotes

- Equipment hours required for each task

- Subcontractor bids for specialty work

The estimate becomes the budget. As work progresses, actual costs get measured against this budget to calculate variances.

Step 3: Track Costs in Real Time

Real-time cost tracking enables proactive management rather than reactive damage control. Contractors who track costs in real time catch overruns earlier than those relying on monthly accounting reports.

Real-time tracking requires daily inputs:

- Time cards submitted by workers each day, coded to specific jobs and tasks

- Material deliveries logged with job numbers and cost codes

- Equipment usage recorded with start/stop times and project assignments

- Subcontractor invoices matched to approved purchase orders

Mobile apps and field management software make this easier. Superintendents can enter costs from the job site rather than relying on office staff to interpret paperwork days later.

Step 4: Analyze Variances and Take Action

Tracking costs without analysis provides no value. The goal is to identify variances while there’s still time to adjust course.

Variance analysis asks three questions:

- What’s the variance? Calculate the percentage difference between estimated and actual costs for each cost code.

- Why did it happen? Investigate the root cause—pricing changes, productivity issues, scope creep, estimation errors, or unforeseen conditions.

- What action is needed? Determine whether the variance can be recovered through efficiency gains, change orders, or value engineering in remaining work.

A 10 percent labor overrun on framing might be offset by scheduling extra crew for remaining phases. Or it might require a conversation with the owner about schedule delays that increased costs.

Benefits of Construction Job Costing

When implemented properly, job costing delivers several strategic advantages beyond basic financial reporting.

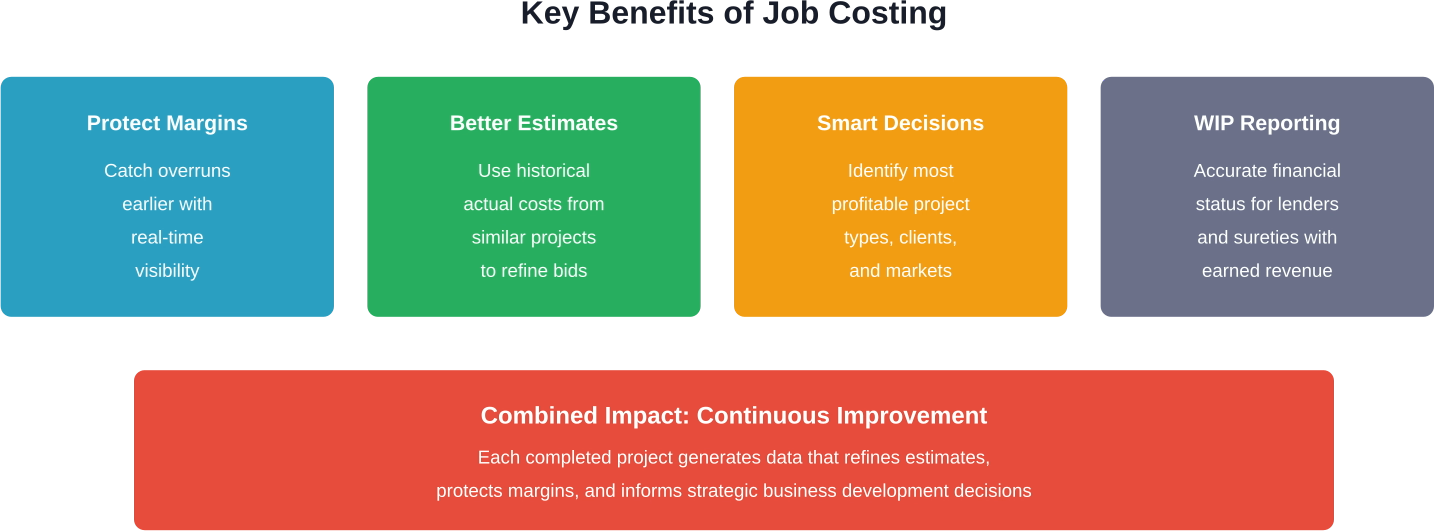

Protects Profit Margins

Profit protection starts with early warning systems. Job costing flags cost overruns before they consume the entire margin.

If a $500,000 project has a 15 percent profit margin, the target profit is $75,000. A 5 percent cost overrun drops that profit to $50,000—a 33 percent reduction in expected return.

But here’s the thing—early detection enables correction. A contractor who spots a 5 percent overrun at 30 percent project completion can implement corrective actions. Waiting until 80 percent completion leaves no room for recovery.

Improves Future Estimating Accuracy

Historical job cost data becomes the foundation for better estimates. Instead of guessing at labor productivity or material quantities, estimators can reference actual performance from similar completed projects.

This creates a continuous improvement cycle. Each completed project generates data that refines the next estimate. Over time, bid accuracy increases and underbidding risk decreases.

Enables Data-Driven Decision Making

Job costing transforms financial data into strategic intelligence. Contractors can identify which project types, clients, or geographic markets generate the best margins.

This informs business development strategy. A contractor might discover that retail tenant improvements consistently outperform residential remodels despite similar revenue. That insight should shape marketing focus and bidding priorities.

Supports Work-in-Progress Reporting

Work-in-Progress (WIP) reports show the financial status of active projects. These reports combine job cost data with percentage-of-completion calculations to determine earned revenue and gross profit.

Lenders and sureties require WIP reports to evaluate contractor financial health. Accurate job costing makes WIP reporting straightforward rather than a monthly struggle to reconcile incomplete data.

Common Job Costing Challenges

Despite its benefits, job costing implementation faces several practical obstacles. Recognizing these challenges in advance helps contractors develop mitigation strategies.

Inconsistent Data Entry

Job costing accuracy depends entirely on consistent, timely data entry. When field crews don’t submit time cards daily or material deliveries aren’t logged with proper cost codes, the system breaks down.

Delayed data entry compounds the problem. Time cards submitted on Friday for the entire week force workers to recall which days they worked on which tasks—memory fails, and accuracy suffers.

Solutions include mobile time-tracking apps that prompt daily submission, simplified cost code structures that reduce confusion, and regular training on proper coding procedures.

Overhead Allocation Disputes

How overhead gets allocated to projects creates ongoing tension. Project managers want minimal overhead burden to make their jobs look more profitable. But company leadership needs accurate overhead allocation to understand true project costs.

The solution is transparency and consistency. Establish a clear overhead allocation method—whether percentage of direct costs, labor hours, or fixed markup—and apply it uniformly across all projects.

Integration With Existing Systems

Many contractors run job costing separately from payroll, accounts payable, and project management systems. This creates data silos and manual reconciliation work.

Integrated construction management platforms solve this by connecting all financial and operational data. Time cards automatically flow into payroll and job costing. Material invoices update both accounts payable and project costs. One data entry serves multiple purposes.

Understanding Markup vs Margin

Contractors frequently confuse markup and margin, leading to underbidding. These terms are not interchangeable.

Markup is the percentage added to costs to determine the selling price. Margin is the percentage of the selling price that represents profit.

The difference matters significantly:

| Markup % | Actual Margin % |

|---|---|

| 10% | 9.1% |

| 15% | 13.0% |

| 20% | 16.7% |

| 25% | 20.0% |

| 30% | 23.1% |

| 40% | 28.6% |

A contractor applying 20 percent markup achieves only 16.7 percent margin. Understanding this distinction prevents margin erosion through miscalculation.

Best Practices for Construction Job Costing

Successful job costing implementations share several common characteristics. These best practices help contractors maximize the value of their cost tracking systems.

Maintain Granular Cost Codes Without Overcomplication

Cost codes need enough detail to provide useful insights without becoming so complex that field teams won’t use them correctly.

A residential contractor might need 50-100 cost codes. A large commercial builder might require 500-1,000 codes to track specialized work across multiple trades and project phases.

The test: Can a field supervisor correctly assign a cost code without consulting a manual? If not, the system is too complex.

Review Job Costs Weekly, Not Monthly

Monthly financial reports arrive too late for effective project management. A cost overrun discovered four weeks after it occurs leaves limited options for correction.

Weekly job cost reviews enable proactive intervention. Project managers can spot unfavorable trends early and adjust labor allocation, material ordering, or work sequences before problems compound.

Calculate and Monitor Labor Burden Accurately

Labor burden rates change throughout the year as insurance premiums adjust, benefit costs increase, and payroll tax caps reset. Using outdated burden rates creates estimation errors.

Calculate burden rates quarterly using actual payroll data. Include all burden components: federal and state payroll taxes, workers’ compensation insurance, general liability insurance, health benefits, retirement contributions, paid time off, and union fringe benefits where applicable.

Build Feedback Loops Between Field and Office

Job costing works best when field teams understand how their daily decisions impact project profitability. Regular communication between project managers and accounting staff creates alignment.

Share weekly cost reports with superintendents. Highlight areas where performance meets or exceeds estimates. Discuss variances collaboratively rather than punitively.

This feedback loop improves future performance. Field teams learn which activities consume budgets quickly and adjust work methods accordingly.

Keep More Profit On Every Job

Job costing doesn’t usually fail in spreadsheets – it fails on site. Hours stretch, sequences shift, and small issues stack up into real cost. By the time it shows in reports, the margin is already gone. Powerkh tracks where that loss actually starts. They compare what was planned with what is being built, highlight where work is drifting, and show which parts of the job are quietly adding time and cost beyond the estimate.

Stop Margin Loss Early

Powerkh helps you tighten job costing by:

- Showing where rework is adding unplanned labor and cost

- Identifying coordination issues that increase installation time

- Highlighting tasks that take longer than expected on site

- Verifying what is actually installed versus what is reported

- Connecting site issues directly to cost impact

If margins are starting to slip, contact Powerkh and take back control before costs get out of hand.

Technology Solutions for Job Costing

Modern construction management software has transformed job costing from a manual accounting exercise into an automated real-time management tool.

Integrated Construction Management Platforms

Comprehensive platforms connect estimating, project management, time tracking, and accounting in a single system. This eliminates data re-entry and ensures consistency across all financial reports.

Key features include:

- Estimate-to-job conversion that establishes cost budgets automatically

- Mobile time cards with GPS verification and photo documentation

- Purchase order management linked to cost codes and budgets

- Real-time dashboards showing cost-to-budget variances

- Work-in-progress reports generated from live data

Many construction business owners report reclaiming significant time per week after implementing integrated systems, allowing them to redirect resources toward project management and business development activities that drive growth.

Mobile Field Applications

Field-based apps put job costing tools directly in the hands of superintendents and foremen. Instead of paper time cards transcribed by office staff, crews enter hours on tablets or smartphones with immediate cost code assignment.

Mobile apps also capture:

- Daily work logs with photos and notes

- Material deliveries with quantity verification

- Equipment usage hours

- Safety incidents and observations

The data flows directly into job costing systems without manual transfer, reducing errors and delays.

Herramientas de colaboración en la nube

Cloud platforms enable real-time access to job cost data from any location. Project managers in the field can check budget status without calling the office. Estimators can review historical costs while visiting a prospective project site.

Cloud systems also simplify multi-project oversight. A contractor running 15 simultaneous jobs can review financial performance across the entire portfolio in minutes rather than waiting for compiled reports.

Moving From Reactive to Proactive Management

The ultimate value of job costing is transformation from reactive to proactive project management. Without job costing, contractors operate blindly until month-end reports reveal problems that occurred weeks earlier.

With effective job costing, decision-making shifts forward. Instead of discovering a $30,000 cost overrun after the fact, project managers see the trend developing and intervene while options still exist.

This shift requires cultural change as much as technological implementation. Field teams must embrace daily cost tracking as part of their workflow. Office staff must prioritize timely data processing over perfection. Leadership must use cost data for improvement rather than blame.

The payoff justifies the effort. Contractors with mature job costing systems consistently outperform competitors on margin preservation, estimate accuracy, and strategic growth.

Conclusión

Job costing transforms construction financial management from guesswork to precision. By tracking actual costs against detailed estimates, contractors gain the visibility needed to protect margins, improve bidding accuracy, and make strategic decisions based on data rather than intuition.

Implementation requires both technology and discipline. Cost codes must be established, estimates must be detailed, and field teams must commit to daily data entry. But contractors who make this investment consistently outperform competitors who rely on basic accounting methods.

The difference between profitable growth and financial struggle often comes down to knowing which jobs make money—before it’s too late to fix the ones that don’t.

Start with one project. Implement proper cost tracking, review variances weekly, and use the insights to improve the next estimate. The compound effect of continuous improvement builds sustainable competitive advantage.

Ready to implement job costing in your construction business? Begin by establishing clear cost codes for your most common project types, then expand the system as your team becomes comfortable with the process.

Preguntas frecuentes

What’s the difference between job costing and project accounting?

Job costing is a specific method within project accounting that tracks costs by individual project. Project accounting is the broader discipline that includes job costing plus revenue recognition, billing, and financial reporting for project-based businesses. Job costing provides the cost data that feeds into comprehensive project accounting.

How often should contractors review job costs?

Weekly reviews provide optimal balance between timeliness and workload. Daily monitoring works for large, complex projects with tight margins. Monthly reviews arrive too late for effective intervention on most construction projects. The goal is catching variances while enough work remains to implement corrections.

Can small contractors benefit from job costing?

Absolutely. Small contractors often benefit more than large firms because they have less margin for error. A single unprofitable project can severely impact a small contractor’s annual performance. Job costing helps small firms identify which project types and clients generate the best returns, enabling focused business development.

What’s a good profit margin in construction?

Typical net profit margins in construction range from 2-10 percent depending on project type, market conditions, and contractor specialization. Residential remodelers often target 8-15 percent gross margins, while large commercial contractors might operate on 3-7 percent net margins with higher volume. Job costing helps contractors understand their actual margins rather than relying on industry averages.

How does job costing handle change orders?

Change orders create separate cost tracking within the job. Most systems allow contractors to budget and track change order costs independently from the base contract, then roll them into total project performance. This preserves visibility into base scope performance while accurately capturing the financial impact of additional work.

What’s the biggest mistake contractors make with job costing?

Inconsistent cost code application undermines job costing accuracy. When field crews assign labor and materials to generic codes like “miscellaneous” instead of specific task codes, the data loses value. The solution is simplified coding structures, regular training, and clear accountability for accurate coding.

Does job costing work for service and maintenance contractors?

Yes, though the approach differs slightly. Service contractors typically track costs by work order or service ticket rather than long-duration projects. The principles remain the same: assign labor, materials, and overhead to specific jobs, compare against estimates or standard rates, and analyze profitability by customer, service type, or technician.

Nuestros casos prácticos

Hemos gestionado más de 200 proyectos BIM y VDC para los sectores comercial, industrial y residencial.

Nuestro trabajo incluye:

Automatización del diseño de encofrados

Our client from

California, USA

Automatización del diseño de falsos techos

Our client from

New York, USA

Automatización del diseño del entramado de muros

Our client from

California, USA