Vous avez des questions ? Contactez nous !

Rejoignez notre équipe !

Demander un devis ou une consultation gratuite

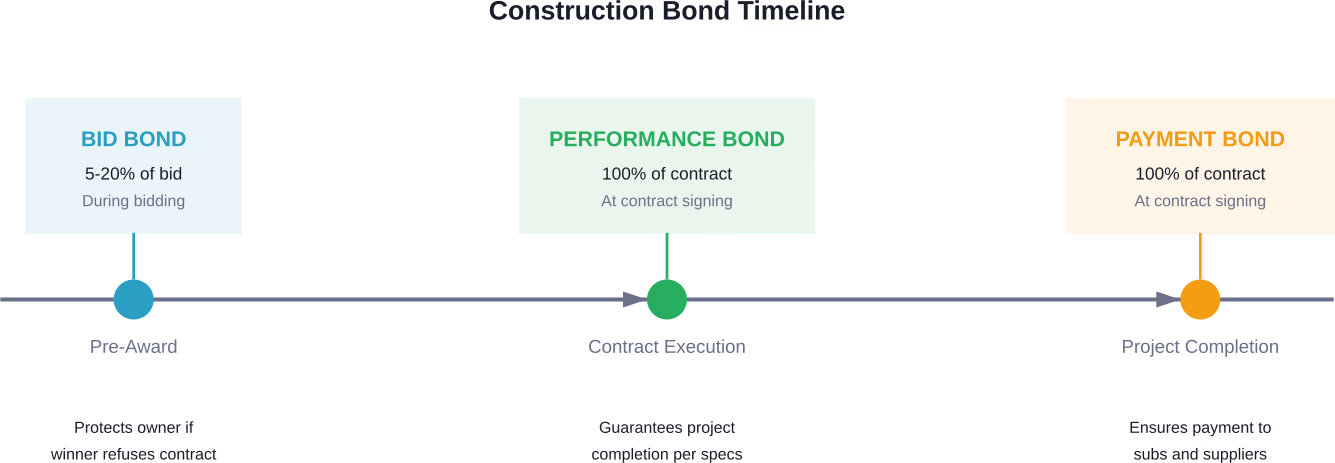

A bid bond in construction is a financial guarantee that protects project owners if the winning bidder refuses to sign the contract or fails to provide required performance and payment bonds. Typically ranging from 5-20% of the bid amount, bid bonds ensure contractors submit serious, financially-backed proposals. The U.S. Small Business Administration guarantees bid bonds for small businesses, while federal projects require at least 20% of the bid price according to the Federal Acquisition Regulation.

Construction bidding involves substantial financial commitments from both contractors and project owners. When contractors submit competitive bids for projects, owners need assurance that winning bidders will actually follow through.

That’s where bid bonds come in. They’re not just bureaucratic paperwork—they’re financial guarantees that separate serious contractors from those who might walk away after winning a bid.

Understanding the Bid Bond Fundamentals

A bid bond is a type of surety bond that guarantees contractors are held accountable for the bids they submit. When contractors compete for construction work, particularly on public projects, they secure bid bonds from surety companies as proof they can honor their bid commitments.

The bond creates a legally binding three-party agreement involving the contractor (principal), the project owner (obligee), and the surety company. If the winning contractor refuses to execute the contract or fails to provide required performance and payment bonds, the surety compensates the owner for the financial difference between the original bid and the next lowest bid.

According to the Federal Acquisition Regulation, government contracts require bid guarantee amounts of at least 20 percent of the bid price but not exceeding $3 million. Private projects typically require 5-10% of the total contract price, though requirements vary based on project scope and owner preferences.

The Three Parties in a Bid Bond Agreement

Every bid bond involves three distinct entities, each with specific roles and responsibilities:

- The Principal: This is the contractor or construction company submitting the bid. Principals apply for bid bonds through surety companies and pay a premium for the guarantee. They’re ultimately responsible for honoring their bid commitments.

- The Obligee: This is the project owner requiring the bond—whether a government agency, private developer, or building owner. The obligee is protected financially if the winning bidder backs out.

- The Surety: This is the bonding company providing the financial guarantee. Surety companies evaluate contractors’ financial strength, experience, and capacity before issuing bonds. If contractors default, sureties pay the obligee and then pursue reimbursement from the contractor.

How Bid Bonds Work in the Construction Bidding Process

The bidding process follows a structured sequence, and bid bonds play a critical role at specific stages.

When project owners decide to solicit competitive bids, they publish bid requirements in their solicitation documents. For government projects, the Federal Acquisition Regulation requires advertising in appropriate venues with specific timeframes. According to AIA Document A701-2018 (Instructions to Bidders), coordinated with AIA Document A201 General Conditions of the Contract for Construction, bonding requirements must be clearly stated in bid solicitations.

Contractors interested in bidding contact surety companies to obtain bid bonds before the submission deadline. The surety evaluates the contractor’s financial statements, work history, and current bonding capacity. For qualified contractors, the surety issues a bid bond for a percentage of the anticipated bid amount.

When Bid Bonds Are Required

Not every construction project requires bid bonds, but certain categories almost always do:

- Government contracts consistently require bid bonds. Federal projects mandate bonds according to the Federal Acquisition Regulation (FAR), which sets specific thresholds for different bond types. State and local requirements vary—for example, Maryland requires bid security equal to at least 5 percent for state construction contracts exceeding $100,000. Arizona law requires bidding and bonding for department facilities involving expenditures of $189,000 or more.

- Large private projects frequently require bid bonds when owners want to ensure serious competition. Developers investing millions in commercial or industrial construction use bid bonds to screen out unqualified or uncommitted contractors.

- Public-private partnerships typically mandate the full suite of construction bonds, including bid bonds, to protect public investment.

The U.S. Small Business Administration guarantees bid bonds for certain small businesses, recognizing that bonding requirements can create barriers to entry for smaller contractors competing for public work.

Bid Bond Amounts and Calculations

Project owners determine bid bond amounts based on project size, complexity, and risk factors. The amount serves as financial protection proportional to the potential loss if a contractor defaults.

For a $500,000 construction bid, a contractor typically secures a bid bond for $25,000 to $50,000 (5-10% of the bid price). Federal projects require at least 20 percent—meaning that the same $500,000 bid would need a $100,000 bid bond for government work.

Here’s the thing though—the bid bond amount isn’t what contractors pay. The bond amount represents the surety’s maximum liability, not the premium cost.

| Project Type | Typical Bond Percentage | Example: $1M Project | Who Sets Requirement

|

|---|---|---|---|

| Federal government | 20% (minimum) | $200,000 bond | Federal Acquisition Regulation |

| State/local government | 5-10% | $50,000-$100,000 bond | State procurement laws |

| Private commercial | 5-10% | $50,000-$100,000 bond | Project owner/developer |

| Small private projects | 0-5% or none | $0-$50,000 bond | Project owner discretion |

What Contractors Actually Pay: Bond Premiums

Contractors don’t pay the full bond amount—they pay a premium, typically 0.5% to 3% of the bond amount depending on their financial strength and track record.

For a $50,000 bid bond, a well-qualified contractor might pay $500-$1,500 in premium. Contractors with weaker financials or limited experience pay higher premiums, sometimes reaching 3% or more.

Surety companies evaluate several factors when setting premiums: credit score, financial statements, years in business, project experience, current work in progress, and available bonding capacity. The stronger the contractor’s profile, the lower the premium rate.

The Relationship Between Bid Bonds and Other Construction Bonds

Bid bonds don’t stand alone in the construction bonding ecosystem. They’re the first in a sequence of bonds that protect project owners through different project phases.

When contractors win bids, they must typically provide two additional bond types: performance bonds and payment bonds. These are often issued together as a “performance and payment bond” package.

Performance bonds guarantee the contractor will complete the work according to contract specifications. The penal sum typically equals 100% of the contract value. If contractors fail to complete the project, the surety either finds a replacement contractor or compensates the owner for completion costs.

Payment bonds (also called labor and material payment bonds) protect subcontractors, suppliers, and laborers. They guarantee payment for work performed and materials delivered. This protects the owner from mechanic’s liens—legal claims against the property for unpaid construction debts.

The bid bond essentially serves as a prequalification step. By securing a bid bond, contractors demonstrate they have sufficient bonding capacity and surety relationships to obtain the required performance and payment bonds if they win.

How to Obtain a Bid Bond

Getting a bid bond requires working with a surety company or surety broker. The process involves financial underwriting similar to applying for a loan, though sureties evaluate different factors.

Start by contacting surety companies or independent surety brokers who specialize in construction bonds. Brokers can shop multiple sureties to find the best rates and terms for specific contractor profiles.

Required Documentation

Sureties typically request comprehensive financial and operational information:

- Three years of audited or reviewed financial statements

- Current work-in-progress schedule showing all active projects

- Personal and business tax returns

- Bank references and credit reports

- Resume of key personnel and organizational structure

- Project experience and reference list

- Equipment ownership and lease schedules

For the specific bid bond application, contractors need the bid solicitation documents, project specifications, bid amount, and project timeline.

Well-established contractors with strong balance sheets can often obtain bid bonds within 24-48 hours. Newer contractors or those with complex financial situations may need several weeks for surety underwriting.

Bonding Capacity Considerations

Sureties don’t issue unlimited bonds. Each contractor has a bonding capacity—the total dollar value of projects they can bond simultaneously—determined by their financial strength.

Generally speaking, bonding capacity relates to working capital and net worth. A common industry guideline suggests contractors can bond projects totaling 10-15 times their working capital, though actual capacity varies based on experience, backlog, and surety relationship.

Contractors need to manage bonding capacity strategically. Submitting bids on too many projects simultaneously can exhaust capacity, preventing them from bonding projects they actually win.

Submit A Bid You Can Back Up

A bid bond means you’re committing to deliver at your price. If scope gaps or coordination issues are hidden, that risk lands on you the moment the bid is accepted. Powerkh checks how the priced scope translates into real work, so you’re not committing to something that will shift later.

Back Your Bid With Real Checks

Powerkh reviews your bid against real project conditions and shows where it can break:

- Where scope is unclear or not fully defined

- Where design and site conditions won’t match

- Which parts of the job rely on assumptions

- Where scope is likely to change after award

- What you’re actually committing to deliver at your price

Contact Powerkh before you submit and make sure your bid holds once it becomes a contract.

What Happens When a Bid Bond Is Claimed

Bid bond claims occur when winning contractors fail to honor their obligations. The consequences extend beyond the specific project.

If a contractor wins a bid but refuses to execute the contract or cannot provide the required performance and payment bonds, the project owner notifies the surety of the default. The surety investigates the claim to verify it’s legitimate.

Valid claims result in the surety paying the obligee the difference between the defaulting contractor’s bid and the next lowest responsive bid, up to the bond’s penal sum. For example, if the winning bid was $1 million, the second-place bid was $1.08 million, and the bond amount was $100,000, the surety pays $80,000 to cover the difference.

But here’s the critical part: Unlike insurance, surety bonds don’t absorb the loss. The surety then pursues the defaulting contractor for reimbursement through the indemnity agreement signed when the bond was issued. This can include legal action to recover the paid amount plus legal fees and interest.

Contractors who default on bid bonds face severe consequences: damaged surety relationships, difficulty obtaining future bonds, reputational harm in the industry, and potential legal liability. The impact can effectively end a contractor’s ability to compete for bonded work.

Bid Bonds vs. Other Bid Security Methods

While bid bonds are the standard for construction, project owners sometimes accept alternative forms of bid security:

- Cashier’s checks or certified checks provide guaranteed funds but tie up contractor capital. For a $50,000 bid security requirement, a contractor must have $50,000 cash available and inaccessible until after bid award—a significant cash flow burden.

- Letters of credit from banks serve as bid security but typically cost more than bid bond premiums and require substantial banking relationships.

- Cash deposits provide the strongest security for owners but create the greatest burden for contractors, essentially removing working capital from circulation.

Bid bonds offer contractors the advantage of securing bid security without tying up capital. The premium cost is far less than depositing the full bond amount, allowing contractors to bid on multiple projects simultaneously.

| Security Type | Contractor Cost | Capital Impact | Common Usage

|

|---|---|---|---|

| Bid bond | 0.5-3% premium | Minimal | Standard for most public and large private projects |

| Cashier’s check | Full amount tied up | High | Small projects or when bonding unavailable |

| Letter of credit | 1-3% annual fee | Medium-High | International projects or special circumstances |

| Cash deposit | Full amount tied up | Very High | Rarely used except for contractors without bonding access |

Why Bid Bonds Matter for the Construction Industry

Bid bonds serve functions beyond protecting individual project owners—they strengthen the entire construction procurement system.

For project owners, bid bonds filter out non-serious bidders. When contractors must secure surety bonds to bid, owners receive proposals only from financially qualified contractors with legitimate intent to perform. This reduces wasted evaluation time on unrealistic bids.

For qualified contractors, bid bonds level the playing field. Without bid security requirements, undercapitalized contractors could submit artificially low bids with no intention or ability to perform, forcing legitimate contractors to compete against unrealistic numbers. Bid bonds ensure all bidders have been vetted by surety companies.

The design-bid-build process, as outlined in AIA standards defining architect’s basic services, relies on competitive bidding producing reliable cost estimates. According to AIA guidance, when Construction Documents are sent out for bid, this phase results in contractors’ final estimates of project costs. Bid bonds ensure these estimates come from contractors who can actually execute at those prices.

For the broader construction industry, bonding requirements promote professionalism and financial responsibility. Contractors who maintain strong surety relationships must demonstrate sound business practices, adequate capitalization, and successful project performance.

Special Considerations for Small Contractors

Bonding requirements can create barriers for small businesses trying to compete for public work. The U.S. Small Business Administration addresses this through its Surety Bond Guarantee Program.

According to the SBA, surety bonds help small businesses win contracts by providing customers with guarantees that work will be completed. The SBA guarantees bid bonds, performance bonds, and payment bonds through its Surety Bond Guarantee Program for small businesses. This significantly expands access to bonded work for emerging contractors.

Small contractors should explore SBA-approved surety programs early in their business development. Building a bonding relationship before it’s urgently needed provides access to larger opportunities as the business grows.

Common Bid Bond Mistakes and How to Avoid Them

Even experienced contractors make bid bond errors that can cost opportunities or create legal complications:

- Waiting until the last minute: Some contractors contact sureties days before bid submission. Surety underwriting takes time, especially for new relationships or complex projects. Contact sureties well in advance of the bid deadline to allow adequate processing time.

- Providing incorrect bond amounts: The bid bond amount must match solicitation requirements exactly. Submitting a bond for 5% when regulations require 10% can disqualify the bid entirely.

- Using non-approved sureties: Government projects require sureties to meet federal bonding requirements.

- Misunderstanding consent of surety requirements: Some contracts require written surety consent before contractors can make certain changes. Proceeding without this consent can trigger bond claims.

- Failing to maintain bonding capacity: Contractors who overextend by bidding too many projects simultaneously may win a bid but find they’ve exhausted bonding capacity and cannot obtain the required performance bond.

The solution? Maintain ongoing surety relationships, understand capacity limitations, carefully review all bid requirements, and allow adequate time for bond procurement.

The Future of Bid Bonds in Construction

Digital transformation is gradually changing how bid bonds are issued and managed, though the fundamental concept remains stable.

Some surety companies now offer digital bond issuance, reducing turnaround time from days to hours. Electronic signatures and digital bond forms streamline the process, particularly beneficial when bid deadlines approach quickly.

Blockchain technology is being explored for bond verification, potentially allowing instant verification of bond authenticity and status without contacting surety companies directly.

That said, the core underwriting process remains relationship-based and document-intensive. Sureties still require detailed financial analysis before extending bonding capacity, and that human evaluation isn’t disappearing soon.

Project owners increasingly incorporate prequalification systems that verify bonding capacity before contractors bid. This front-loads the bonding verification process, reducing bid day complications.

Conclusion

Bid bonds represent more than bureaucratic requirements—they’re fundamental mechanisms that make competitive construction bidding work for everyone involved.

For project owners, bid bonds provide financial protection and ensure only qualified contractors compete. For qualified contractors, they create level playing fields and demonstrate professional credibility. For the construction industry broadly, they promote financial responsibility and professional standards.

Understanding bid bonds—how they work, what they cost, and how to obtain them—is essential for contractors pursuing public work and large private projects. The Federal Acquisition Regulation, state procurement laws, and industry standards like AIA contract documents all recognize bid bonds as standard practice for good reason.

Contractors should establish surety relationships early, maintain strong financial practices, and manage bonding capacity strategically. These steps ensure bid bonds enhance rather than limit competitive opportunities.

Whether bidding your first public project or managing an established construction business, bid bonds are tools that demonstrate your commitment, capacity, and credibility. Master this aspect of construction contracting, and doors to larger, more profitable projects open accordingly.

Questions fréquemment posées

How much does a bid bond cost?

Bid bond premiums typically range from 0.5% to 3% of the bond amount, not the project cost. For a $50,000 bid bond (on a $500,000 project), contractors with strong financials might pay $250-$500, while those with weaker profiles could pay $1,500 or more. The exact premium depends on the contractor’s credit, financial strength, experience, and relationship with the surety.

Is a bid bond refundable if you don’t win the project?

The premium paid for a bid bond is not refundable, regardless of whether the contractor wins the bid. This is standard for all surety bonds – the premium pays for the surety’s guarantee during the specified period. Contractors who bid frequently factor bond premiums into their bidding costs and business development budgets.

What’s the difference between a bid bond and a performance bond?

A bid bond protects owners during the bidding phase if the winning contractor refuses to sign the contract. A performance bond protects owners during construction if the contractor fails to complete the work according to specifications. Bid bonds are typically 5-20% of the bid amount, while performance bonds are usually 100% of the contract value. Contractors need bid bonds to submit bids and performance bonds to execute contracts.

Can you get a bid bond with bad credit?

Getting bid bonds with poor credit is challenging but not impossible. Sureties evaluate multiple factors beyond credit scores, including work history, financial statements, and project experience. Contractors with credit issues might access bonding through the SBA Surety Bond Guarantee Program, though they’ll likely pay higher premiums. Building relationships with specialized sureties who work with emerging contractors can also help.

How long does it take to get a bid bond?

For contractors with established surety relationships, bid bonds can be issued within 24-48 hours. First-time bond applicants should allow 2-4 weeks for the complete underwriting process, as sureties need time to review financial statements, verify references, and assess bonding capacity. Urgent situations might be accommodated faster, but adequate planning prevents last-minute complications.

What happens to the bid bond after you win the contract?

Once the winning contractor signs the contract and provides the required performance and payment bonds, the bid bond obligation is released. The bid bond essentially converts into the performance bond. If the contractor cannot provide performance and payment bonds after winning, the bid bond is forfeited and the surety pays the owner according to the bond terms.

Are bid bonds required for private construction projects?

Private project owners have discretion whether to require bid bonds. Large commercial developers often require them to ensure serious competition, while smaller private projects might not. Government projects almost always require bid bonds above certain dollar thresholds. When bidding private work, carefully review the Instructions to Bidders to determine bonding requirements before preparing proposals.

Nos études de cas

Nous avons géré plus de 200 projets BIM et VDC pour les secteurs commerciaux, industriels et résidentiels.

Notre travail comprend

Automatisation de la conception des coffrages

Our client from

California, USA

Automatisation de la conception des plafonds suspendus

Our client from

New York, USA

Automatisation de la conception de l'ossature des murs

Our client from

California, USA