هل لديك أي أسئلة؟ اتصل بنا!

انضم إلى فريقنا!

اطلب عرض أسعار أو استشارة مجانية

Overhead in construction refers to the indirect costs of running a construction business that aren’t tied to a specific project—like office rent, utilities, insurance, administrative salaries, and equipment maintenance. These ongoing expenses exist whether a company has one job or twenty, and they must be calculated and allocated to projects to ensure accurate bidding and profitability.

Construction companies face a complex financial landscape. Beyond the obvious costs of materials and labor for each project, there’s a hidden layer of expenses that can make or break profitability.

These are overhead costs. And understanding them isn’t optional—it’s essential for survival.

Many contractors discover this the hard way. One contractor shared their experience: “I didn’t understand what my overhead was. I was getting 90% of the jobs I bid, and I thought I was just the world’s greatest businessman. The reality was I was undercharging for really good quality work.”

That story isn’t unique. Construction costs go beyond materials and wages, and failing to account for overhead properly leads to thin margins or outright losses.

Understanding Overhead in Construction

Overhead refers to ongoing expenses incurred by a construction company that aren’t directly tied to a specific project. These are the costs that keep the lights on and the business running.

Think of it this way: when a contractor frames a house, the lumber and the carpenter’s wages are direct costs. The office is rented back at headquarters? That’s overhead.

Overhead costs are related to project expenses that are associated with running operations from the main office. These expenses exist regardless of whether the company has one active project or a dozen.

Direct Costs vs. Indirect Costs

The distinction matters for accurate job costing and bidding.

Direct costs can be traced to a specific project: materials purchased for that job, labor hours worked on site, equipment rentals for that particular build. These costs appear on individual job cost reports.

Indirect costs—overhead—serve the entire business operation. They can’t be neatly assigned to a single project without some form of allocation method.

According to Washington Administrative Code § 296-17A-0510, wood frame building construction includes framing activities such as roof truss placement, roof sheathing, exterior siding installation, door and window installation, and log home shell erection. But the administrative staff processing those invoices? That’s overhead.

Common Types of Construction Overhead Costs

Overhead expenses vary by company size and business model, but most construction firms share similar categories.

General and Administrative Expenses

Office rent or mortgage payments for the main office and any satellite locations represent significant fixed overhead. Utilities for these spaces—electricity, water, internet, phone systems—add up monthly.

Administrative salaries for staff who don’t work on job sites fall into this category: accountants, project managers working from the office, receptionists, HR personnel, and estimators.

Office supplies, computers, software subscriptions, and furniture also count as overhead.

Insurance and Professional Services

General liability insurance, workers’ compensation insurance, professional liability coverage, and vehicle insurance protect the business but don’t tie to individual projects.

Legal fees, accounting services, and consulting expenses serve the entire operation. These professional services keep the company compliant and running smoothly.

Marketing and Business Development

Website hosting and maintenance, advertising costs, trade show participation, and business development activities attract new clients but can’t be billed to current projects.

Some companies include vehicle expenses for company trucks used by management, along with fuel and maintenance costs that aren’t job-specific.

Equipment and Depreciation

Equipment maintenance and repairs for tools shared across multiple projects count as overhead. Depreciation on owned equipment represents the gradual loss of value over time.

Small tools and supplies that serve multiple jobs rather than being purchased for specific projects fall into this category as well.

How to Calculate Construction Overhead

Accurate overhead calculation drives competitive pricing and healthy profit margins. The process requires tracking and categorization.

Step 1: Identify All Overhead Expenses

Review financial statements for a complete accounting period—typically a year. List every expense that isn’t directly tied to a specific project.

Include fixed costs like rent and insurance. Add variable costs like utilities and office supplies. Don’t forget depreciation and less obvious expenses like professional development or trade association dues.

Step 2: Calculate Total Overhead Costs

Sum all identified overhead expenses for the period. This gives the total overhead burden the business carries.

For example, if annual overhead expenses total $240,000, that’s the baseline figure needed for allocation.

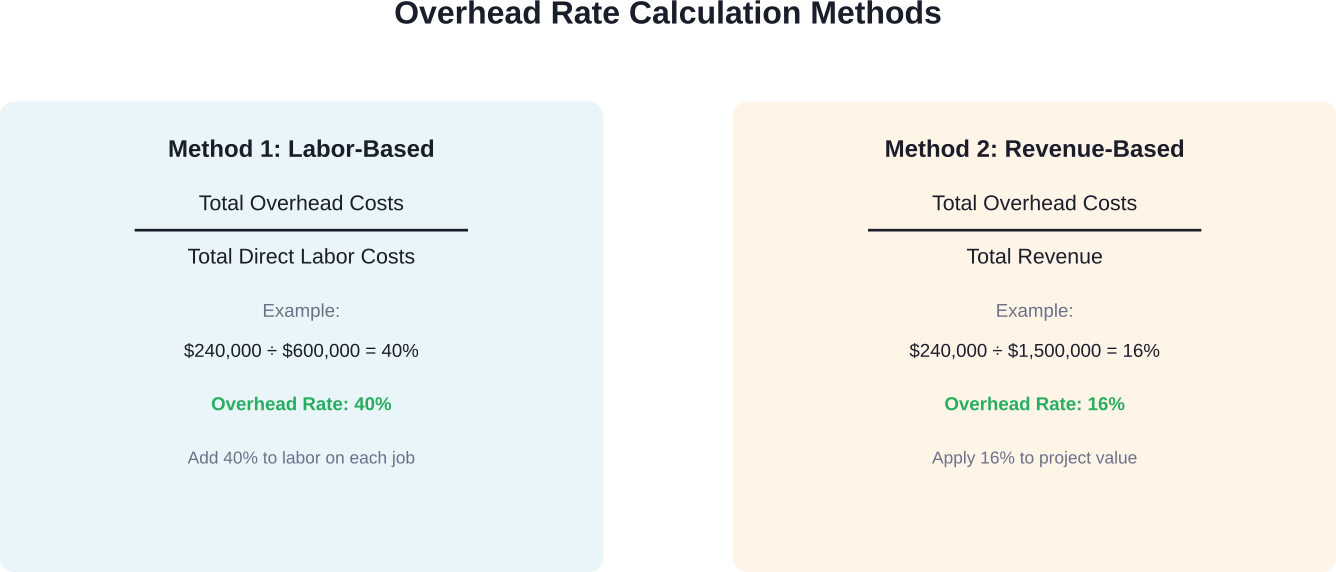

Step 3: Determine Your Overhead Rate

The overhead rate expresses overhead as a percentage of another metric—usually direct labor costs or total revenue.

Calculate the overhead rate by dividing total overhead costs for a specific period by the total quantity of the chosen allocation base.

If total overhead is $240,000 and total direct labor costs are $600,000, the overhead rate is 40% ($240,000 ÷ $600,000 = 0.40).

Some companies prefer calculating overhead as a percentage of total revenue. If annual revenue is $1,500,000, overhead represents 16% of revenue ($240,000 ÷ $1,500,000 = 0.16).

Overhead Cost Allocation Methods

Once overhead costs are calculated, they need to be distributed across projects. This process—overhead cost allocation—ensures each job bears its fair share of indirect expenses.

Labor-Hour Allocation

This method assigns overhead based on labor hours worked on each project. If a project consumes 100 hours out of 2,000 total company labor hours, it receives 5% of total overhead costs.

Labor-hour allocation works well for companies where overhead correlates closely with workforce activity.

Direct Labor Cost Allocation

Similar to labor-hour allocation, but based on labor dollars rather than hours. A project with $30,000 in direct labor costs would receive proportionally more overhead than one with $15,000 in labor.

This approach recognizes that higher-skilled, higher-paid workers may generate more overhead consumption.

Revenue-Based Allocation

Some firms allocate overhead as a percentage of project value. A $200,000 project receives twice the overhead allocation of a $100,000 project.

This method is straightforward but may not reflect actual overhead consumption patterns across different project types.

Activity-Based Costing

More sophisticated companies use activity-based costing, which assigns overhead based on the specific activities that drive costs. A project requiring extensive estimating time, permitting work, or equipment usage receives overhead allocation reflecting those demands.

Activity-based costing provides greater accuracy but requires more detailed tracking systems.

Cut Overhead Before It Stacks Up

Overhead doesn’t spike overnight – it builds when the job drags. Extra supervision, extended site setup, more coordination time. All of it comes from work not moving as planned. باورخ targets that slowdown at its source by checking how design and coordination are holding up once construction begins. By showing where progress will stall and where effort is being wasted, Powerkh helps you stop overhead from quietly growing in the background.

Keep Overhead From Growing

Where Powerkh makes a direct impact:

- Shows where site progress is slowing down and why

- Identifies coordination issues that extend project duration

- Highlights areas causing repeated effort and supervision

- Flags delays that increase time-related overhead

- Keeps work aligned so timelines don’t stretch unnecessarily

If overhead is climbing without clear reason, contact Powerkh and stop it before it builds into your cost.

Understanding Profit Margin in Construction

Overhead is just one piece of the pricing puzzle. The other critical component is profit margin—the percentage added to cover overhead and generate net profit.

According to industry data, general and prime contractors typically achieve gross profit margins of approximately 20–22% and net profit margins of 10–12%. Single-family residential builders average around 21% gross profit and 9% net profit.

But here’s the thing: these are averages. Individual companies vary widely based on market conditions, efficiency, and pricing strategy.

| Contractor Type | Average Gross Profit Margin | Average Net Profit Margin |

|---|---|---|

| General/Prime Contractors | 20–22% | 10–12% |

| Single-Family Residential Builders | ~21% | ~9% |

| U.S. Construction Industry Average | Varies by sector | ~8–12% |

Markup vs. Margin

Many contractors confuse markup and margin. They’re not the same.

Markup is added to costs. A 20% markup on $100,000 in costs equals $120,000 in price.

Margin is calculated from the selling price. A 20% margin on a $120,000 project means $24,000 in gross profit.

Understanding this distinction prevents underpricing. A 20% markup doesn’t deliver a 20% margin—it delivers approximately 16.7% margin.

Strategies to Manage and Reduce Overhead

High overhead erodes profitability. Smart contractors actively manage these costs without compromising business quality.

Implement Time Tracking Systems

Accurate time tracking for administrative and field personnel reveals where overhead accumulates. Software solutions automate this process and improve allocation accuracy.

Better data leads to better decisions about staffing and resource deployment.

Review Insurance Costs Regularly

Insurance represents a significant overhead expense. Shopping carriers annually and implementing safety programs can reduce premiums without sacrificing coverage.

Bundling policies and maintaining clean claims histories also help control costs.

Optimize Office Space

Real talk: do you need that much office space? Strategic space reductions through remote work arrangements and shared office solutions can significantly reduce rent and utility expenses.

Automate Administrative Tasks

Technology reduces manual administrative work. Automated invoicing, digital document management, and integrated project management systems decrease the labor hours needed for overhead functions.

The upfront investment in software often pays for itself within months through reduced administrative staffing needs.

Accurate Job Costing

Tracking labor costs, managing overhead allocation, and improving job costing in construction projects prevents financial losses. Many contractors lose money on projects without realizing it because their overhead allocation is inaccurate.

Regular job cost analysis identifies which project types are actually profitable after true overhead costs are considered.

Common Overhead Mistakes Contractors Make

Even experienced contractors sometimes stumble with overhead management.

Underestimating True Overhead

Forgetting to include all indirect costs leads to artificially low overhead rates. That means underbidding projects and wondering why profits disappear.

Community discussions among contractors frequently mention discovering hidden overhead expenses that weren’t being tracked or allocated properly.

Using Outdated Overhead Rates

Business expenses change over time. Using last year’s overhead rate when costs have increased means each new project fails to recover current indirect costs.

Overhead rates should be recalculated at least annually, preferably quarterly for rapidly growing companies.

Failing to Separate Overhead from Profit

Some contractors lump overhead and profit together as a single markup percentage. This approach obscures whether jobs are actually covering indirect costs.

Separating overhead recovery from profit margin provides clarity. First, ensure overhead is covered. Then, add profit on top.

Inconsistent Allocation

Applying overhead haphazardly across projects—allocating more to some jobs and less to others without a systematic method—creates distorted profitability pictures.

Consistency in allocation methodology ensures comparable data for evaluating project performance.

The Role of Contingency in Project Budgeting

While not technically overhead, contingency allowances relate to risk management in construction budgeting.

According to AIA resources on contingency management, a contingency is a predetermined amount or percentage of the contract held for unpredictable changes in scope or unforeseen conditions.

According to AIA resources on contingency management, most errors and omissions amount to less than 5 percent of a project’s budget. Owner program changes inevitably occur during a project’s life, and modifications or scope adjustments need financial cushioning.

Properly managed contingencies mitigate risk and provide safeguards for designers, contractors, and owners to complete projects on budget.

Taking Control of Construction Overhead

Understanding overhead transforms how construction businesses approach pricing, bidding, and profitability. It’s not the most exciting aspect of running a contracting company, but it’s absolutely foundational.

The contractors who thrive aren’t necessarily those who win the most bids. They’re the ones who understand their true costs, allocate overhead accurately, and price projects to ensure both overhead recovery and genuine profit.

Start by identifying all overhead expenses. Calculate an accurate overhead rate using a methodology that fits the business model. Apply that rate consistently across all projects. Then track actual performance against projections to refine the approach over time.

Here’s what happens when overhead is managed properly: bidding becomes more confident, profit margins improve, cash flow stabilizes, and the business becomes genuinely sustainable rather than just busy.

Don’t repeat the mistake of winning 90% of bids while undercharging for quality work. Know the numbers. Price accordingly. Build a profitable construction business that lasts.

الأسئلة الشائعة

What is the difference between overhead and direct costs?

Direct costs are expenses directly traceable to a specific project, like materials purchased for that job, labor hours worked on site, or equipment rented specifically for that build. Overhead costs are indirect expenses that support the entire business operation but can’t be tied to a single project – such as office rent, administrative salaries, insurance, and utilities.

What is a typical overhead percentage for construction companies?

Overhead as a percentage of revenue typically ranges from 10% to 25% for construction companies, depending on company size, market, and business model. Smaller operations often run leaner with overhead around 10-15%, while larger firms with more administrative infrastructure may see 20-25%. The key is knowing your specific overhead rate and ensuring it’s covered in project pricing.

How often should I recalculate my overhead rate?

Overhead rates should be recalculated at least annually to reflect current business expenses. However, companies experiencing rapid growth, significant changes in staffing, or major shifts in operational costs should recalculate quarterly. Using outdated rates leads to underbidding and eroded profit margins as actual overhead expenses exceed what’s being recovered from projects.

Should overhead and profit be calculated separately?

Yes. Calculating overhead and profit as separate components provides clarity and ensures both indirect costs and actual profit are adequately covered. Overhead represents cost recovery for running the business, while profit is the return on investment and risk. Lumping them together makes it difficult to determine whether projects are truly profitable or merely breaking even after overhead.

What’s the difference between markup and margin in construction pricing?

Markup is a percentage added to total costs to determine the selling price. Margin is a percentage of the selling price that represents profit. A 20% markup on $100,000 in costs yields a $120,000 price, but that’s only a 16.7% margin ($20,000 profit ÷ $120,000 price). Understanding this distinction prevents underpricing – contractors need to calculate which markup percentage delivers their target margin.

How can I reduce my construction overhead without hurting the business?

Focus on efficiency rather than cutting essential services. Implement time tracking to identify waste, automate administrative tasks with software, review and negotiate insurance costs annually, optimize office space through remote work or shared arrangements, and regularly audit subscriptions and services to eliminate unused expenses. Technology investments often reduce long-term overhead by decreasing manual labor needs.

What allocation method works best for construction overhead?

The best allocation method depends on what drives overhead consumption in a specific business. Labor-hour or direct labor cost allocation works well for companies where workforce activity correlates with overhead. Revenue-based allocation suits firms with relatively consistent project types. Activity-based costing provides the most accuracy but requires detailed tracking. Choose a method that’s sustainable for your systems and reflects how overhead is actually consumed.

دراسات الحالة لدينا

لقد تعاملنا مع أكثر من 200 مشروع من مشاريع نمذجة معلومات المباني ونمذجة معلومات المباني للقطاعات التجارية والصناعية والسكنية.

يشمل عملنا ما يلي:

أتمتة تصميم القوالب

Our client from

California, USA

أتمتة تصميم السقف المعلق

Our client from

New York, USA

أتمتة تصميم إطارات الحائط

Our client from

California, USA